")

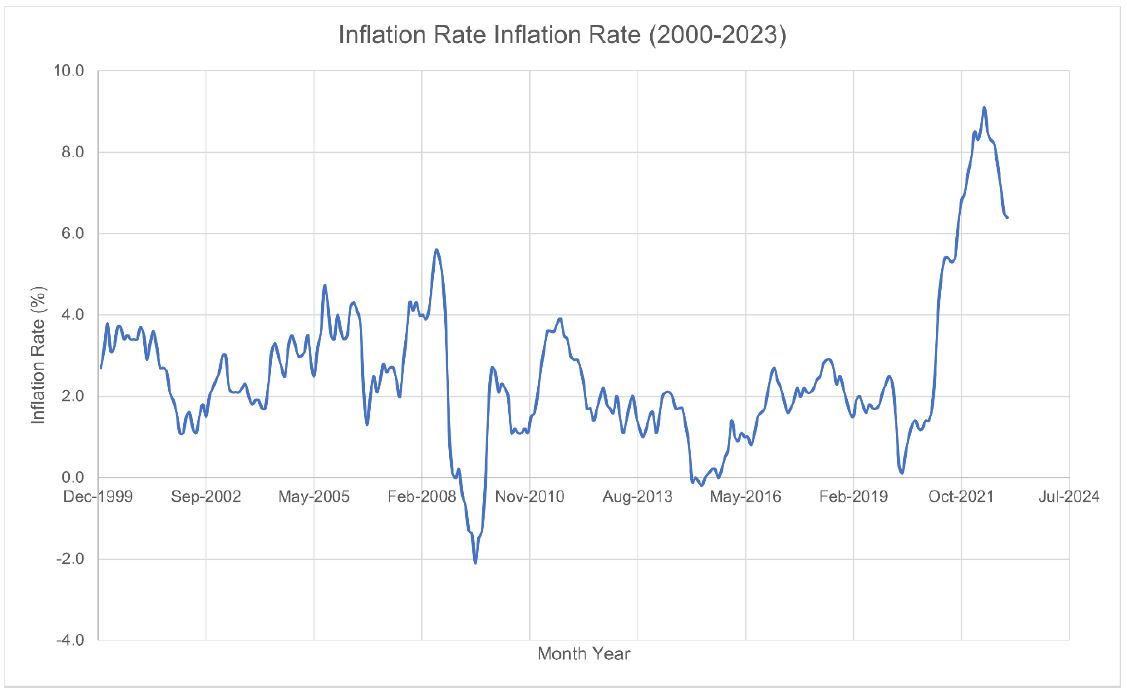

Consumer prices in the United States (US) dipped from 6.5% in December 2022 to 6.4% in January 2023, beating analysts’ forecasts of 6.2%, and raising concerns whether interest rates pivot will come anytime soon.

The US inflation rose by 0.5% from 0.1% in December, partly reflecting an uptick in energy prices while the core number which takes out volatile items like energy and food increased by 0.4%.

The year-on-year core figure recorded 5.6% (without energy and food), down from 5.7% in the prior month, also ahead of the predictions of 5.5%.

Inflation in the US has been falling for seven months straight, after it peaked at 9.1% in June 2022.

Possible impact on interest rates

On Feb 1, the US Fed raised benchmark lending rates by 25 basis points from 4.75% to 4.50% to rein in cost as inflation began to show signs of cooling.

Although the Fed Chair, Jerome Powell, admits inflation has eased somewhat, he believes there is a need for further hikes till inflation hits the 2% target.

The increase in labour statistics in January 2023 and the recent inflation of 6.4% signal that inflation may take longer than previously anticipated to come down to 2%.

However, with the US economy heading towards a recession, the Fed will be more cautious when raising interest rates. A hawkish policy will likely cause the US economy to cave into recession.

The Fed will increase the rates possibly by a quarter basis point at its next meeting in March 2023 and move gradually till there is a soft landing.

What does this mean for the SSA Eurobond Market?

Although the January 2023 inflation figure didn’t reduce at the pace analysts predicted, inflation is still expected to drop further in the coming months.

Despite the current volatility in the SSA Eurobond market, the bear market will continue to run for a couple of months due to inflationary risks and the outlook for the SSA economy for the year.

A lot of the volatility in the market so far is because traders and investors have been pricing bonds on the expectation that revenue and growth will slow over the coming year.

However, the uncertainties with Nigeria’s election will soon be over when a new leader is elected. Ghana is gradually making progress with its debt restructuring and Kenya’s new budget is looking at boosting revenue and reducing debt levels. The war in Ethiopia is also over, and the country’s economy is set to grow at 7% in 2023.

These developments, coupled with a reduced US inflation means there is light at the end of the tunnel and risk assets will eventually rally this year.

It makes sense that investors will want to limit their exposure in the current volatile market. However, investors sitting on the sidelines, waiting for the perfect time to get in can miss out on the gains when the market begins to rally.