")

Low capital buffers mean many Moroccan banks are susceptible to economic volatility, particularly in light of their weak asset quality and above-average risk appetite, Fitch Ratings says.

Tangible common equity averages about 10% of tangible assets for the major Moroccan banks - a limited buffer given the banks' risk profiles, single-obligor concentration risk and possible under-reporting of loan impairments.

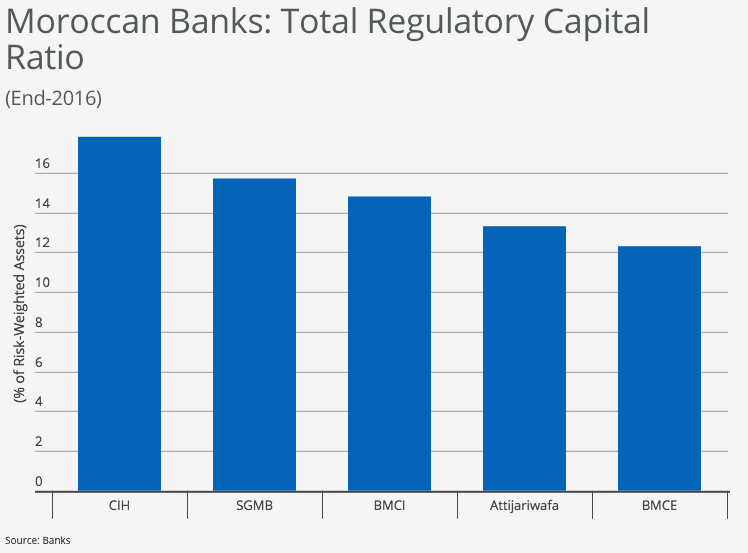

The Fitch Core Capital/weighted-risks ratios for rated banks averaged 12.6% at end-2016 but there is wide variation among banks. The lower ratios for Attijariwafa Bank (10.8%) and Banque Marocaine du Commerce Exterieur (BMCE; 9.7%) highlight their vulnerability to even moderate shocks, which weighs on their Viability Ratings ('bb-' and 'b+', respectively). Total regulatory capital ratios, supported by subordinated debt, give a similar picture, with Attijariwafa (13.3%) and BMCE (12.3%) only marginally above the 12% regulatory minimum.

Reported impaired loans to total loans ratios are considerably higher in Morocco than in developed markets. The average for Morocco's seven largest banks was 9.7% at end-2016, 70% reserved, and we believe local reporting practices understate the true extent of asset quality weakness. Societe Generale Marocaine de Banques (SGMB) and Banque Marocaine pour le Commerce et l'Industrie (BMCI), which follow more conservative classification policies imposed by their French parent banks, reported significantly higher ratios of 14.6% and 12.7%, respectively. We estimate that impaired loans would represent 12%-14% of sector loans if we were to include under-reported impairments as well as watch list, restructured and foreclosed loans.

Moroccan banks typically have a higher risk appetite than the banks we rate in developed markets. Their underwriting standards can become more relaxed as they adapt to local market conditions when opportunities for sound lending become limited and competition intensifies. The country's three largest banks are expanding into other African markets, which involves exposure to domestic sovereign bonds rated significantly lower than Moroccan sovereign bonds (BBB-) and riskier operating environments - a drag on their credit profiles.

Attijariwafa and BMCE are domestic systemically important banks and their 'BB+' Long-Term Issuer Default Ratings are driven by our view of likely support from the Moroccan state, if needed. Credit Immobilier et Hotelier's (CIH) ratings reflect our view of likely support, if needed, from its majority owner, a leading public-sector investor focused on Morocco's economic development. CIH is Morocco's specialist retail mortgage and commercial real estate lender. The ratings of SGMB and BMCI reflect our view of likely support from majority owners, Societe Generale and BNP Paribas, respectively, if needed.