")

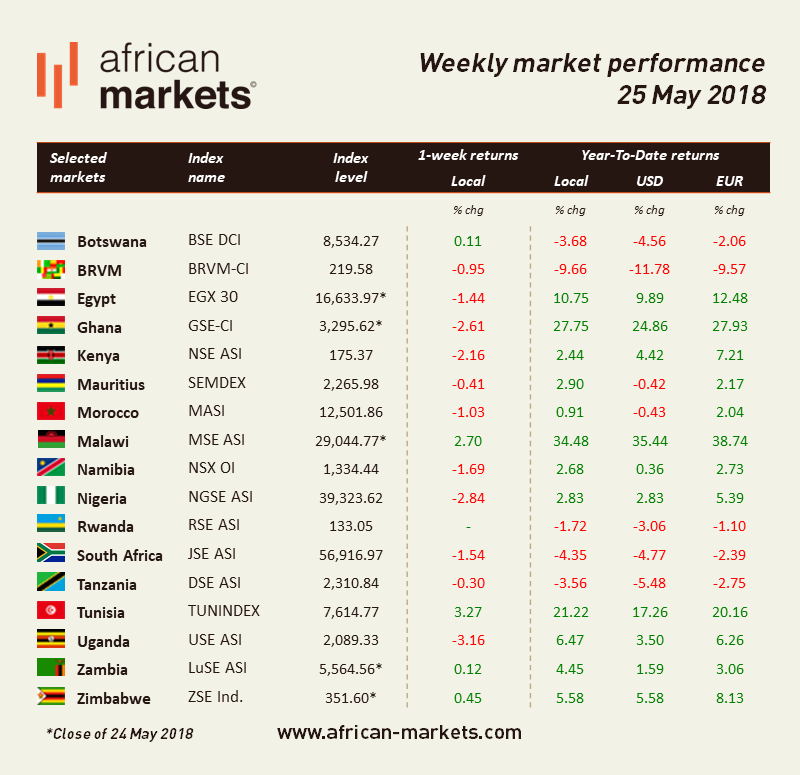

It was a tough week on African markets with most of the markets under coverage closing on negative territories. Tunisia is this week’s best performer closely followed by Malawi.

S&P affirmed South Africa’s sub-investment grade credit rating and kept its stable outlook. S&P rates the country’s foreign currency debt ‘BB’ and its local currency debt ‘BB+’, having downgraded the country to “junk” last year as the economy and public finances weakened under Zuma. The stable outlook is based on the agency’s view that South Africa’s economic growth would humbly take up over the next year following economic and social reforms undertaken by the new administration. Sentiment has turned positive on South Africa since President Cyril Ramaphosa has pledged to undertaken necessary fiscal and economic reforms. In other news, as expected, the SARB decided to keep the repurchase rate unchanged at 6.5% stating however that in contrast with the previous meeting, the committee assessed the risks to the inflation forecast to have moved to the upside. The central bank said consumer price inflation is expected to average 4.9% this year, rising to 5.2% in 2020 which remains within the bank’s target range. The JSE lost 1.54%.

The NGSE lost 2.84%. The Nigerian index has plunged to a level not seen since in January. Yields on Nigeria’s treasuries have plummeted to around 12% from 18% a year ago due to government initiative to cut borrowing costs and U.S. interest rate increases. This has prompted investors to retire from local assets. Banking and consumer stocks were particularly hit. In parallel, Nigeria’s central bank kept its main interest rate unchanged at 14% which surprised given decelerating inflation. Governor Godwin Emefiele stated that “the objective of the policy stance will be to accelerate the reduction in the rate of inflation to single digits, promote economic stability, boost investor confidence and promote foreign capital flows”. The bank still sees to inflation outlook following the influx of cash from the implementation of Nigeria’s 2018 budget and potential heavy spending during upcoming elections. This comes as latest data showed a slight deceleration in the economic growth trends with GDP growing 1.95% in the first quarter of 2018 lifted by the oil sector compared to 2.11% year-on-year in the final quarter of 2017.

As widely anticipated given latest data, Ghana’s central bank cut its benchmark interest rate by 100 basis points to 17% on Monday. Central Bank Governor Ernest Addison projected that inflation would fall to the bank’s target of 8% by the end of this year or early 2019. Annual inflation fell to 9.6% in April from 10.4% the month before. Indeed there have been signs of economic stabilisation in Ghana which bode well for the bank’s decision. Ghana’s statistic office reported that the country’s producer price inflation rose to 6.4% year-on-year in April from 3.7% in March. The GSE shed 2.61%.

Malawi’s agriculture Minister reported that the country’s maize output declined by 19.4% in the 2017/18 farming year to 2.8 mn tons due to damage caused by drought and crop-eating armyworms. There could be substantial reductions in the yields of most of Malawi’s major food crops i.e. cassava, groundnuts and sorghum. This could have an adverse effect on Malawi’s economy which relies heavily on rain-fed agriculture. The MSE added 2.7%.