")

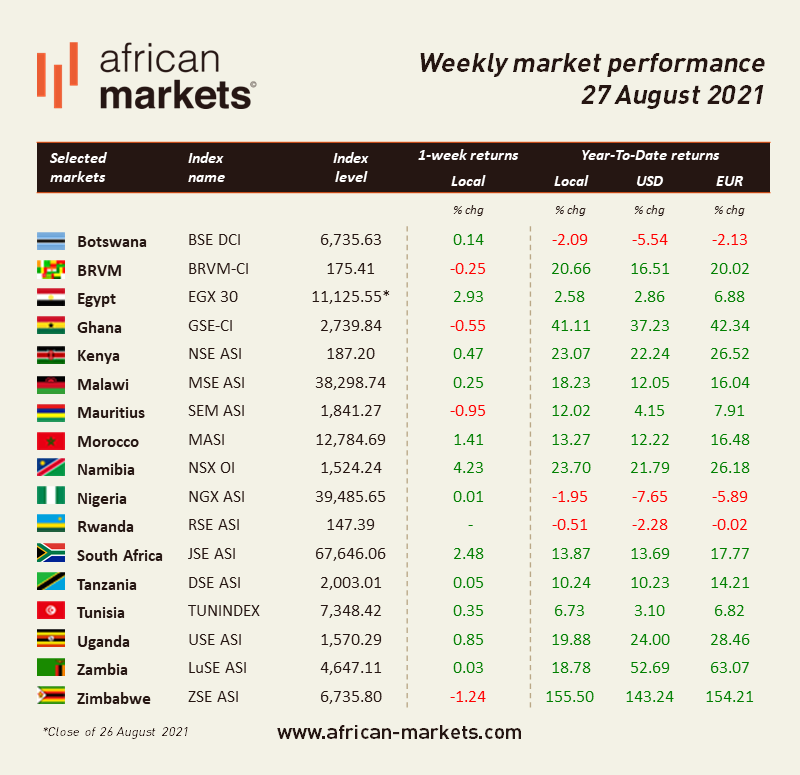

The sentiment was mainly positive on African equity markets this week. Among the 17 markets we cover, twelve advanced while four retreated and one remained flat. The Namibian Stock Exchange led the pack as equities in Windhoek rallied 4.23%. Conversely, the Zimbabwe Stock Exchange was the laggard. Zimbabwean equities shed 1.24% this week, the most on the continent.

West Africa

BRVM - Equities in Abidjan cooled down this week after seven consecutive weeks of positive performance. Overall, the Composite Index shed 0.25% WoW to close at 175.41. Market activity declined 8% as XOF 374m (USD 0.67m) worth of shares changed hands every day on average compared to XOF 407m the week before. The market is now up 20.66% year-to-date, and the total market capitalisation amounts to XOF 5,279bn (USD 9.46bn). Sucrivoire SA is the top performer this week. Shares in the sugar producer soared 24.8% and are up 180% YTD. The market heavyweight, Sonatel, closed lower at XOF 13,795 on Friday (-1.46% WoW) and is now up 2.19% since the start of the year.

NGX - Equities in Lagos remained flat this week. The NGX ASI, the benchmark index of the Nigerian exchange, edged up a mere 0.01% WoW, closing on Friday at 39,485.65. Stocks are now down 1.95% YTD. Activity declined 23% as NGN 1.6bn (USD 3.98m) worth of shares were traded daily on average over the week. The total market capitalisation stands at NGN 20.6tn (USD 50.0bn). UACN Property Development is the top performer. Shares in the property developer jumped 37.6% and are now up 131.65% YTD. The market heavyweight, Dangote Cement, remained flat at NGN 249.6 on Friday and is up 1.92% YTD.

North Africa

BVC - Moroccan equities rallied as the MASI rose 1.41% WoW. Market activity increased 5.5% as MAD 74m (USD 8.3m) worth of shares changed hands every day on average compared to MAD 70m the week before. The total market capitalisation stands at MAD 656.2bn (USD 73.12bn), up 13.27% YTD. M2M Group is once again among the top performers this week. Shares in the technology company that provides processing solutions, securities management, and other electronic services advanced another 7.9% and are now up 20.13% YTD. The heavyweight, Maroc Telecom, closed at MAD 141 on Friday (up 1.40% WoW). The stock is down 2.76% YTD.

EGX - Egyptian equities closed higher this week. The EGX 30 rallied 2.93% and closed at 11,125.55 points on Thursday. Compared to the previous week, the average daily turnover increased 13% at around EGP 2.2bn (USD 138.89m), and the total market capitalisation amounts to EGP 732.7bn (USD 46.7bn). The benchmark index is now up 2.58% YTD. El Shams Housing and Urbanization SAE is once again among the top performers. Shares in the real estate developer jumped another 50.6% WoW and are now up 2554.75% YTD. The Egyptian heavyweight, CIB, closed at EGP 47.18 (+3.94% WoW) on Thursday. Shares are now up 6.28% since the start of the year when adjusted for the capital increase. Fawry, the listed fintech company, closed the week at EGP 16.18 (down 3.23% WoW).

East Africa

NSE - Bullish sentiment prevailed in Nairobi. The NSE ASI gained another 0.47% WoW to close at 187.20. The average daily turnover dropped 48.5% to KES 470.6m (USD 4.28m), and the total market capitalisation amounts to KES 2,917.37bn (USD 26.56bn). The market is up 23.07% YTD. KenGen is among the best performers this week. The shares in the utility company rose 9.58% WoW as it reported a key milestone in the ongoing USD 6.2m geothermal drilling contract in Ethiopia. Indeed, it announced that its team of engineers have so far crossed the 450 meters of a drilling depth (the most difficult part) of the first of eight geothermal wells for the state-owned electricity producer, Ethiopia Electric Power Company. It projects it will complete drilling of that first well within two months. The counter is now up 4.46% YTD. Safaricom closed at 44.35 KES (down 0.22% WoW). Shares are up 29.49% so far this year.

Southern Africa

JSE - South African equities rallied this week. The JSE ASI rose 2.48% WoW to close at 67,646.06, with the best performances coming from precious metals, resources and banks, which gained 5.69%, 4.64% and 4.57%, respectively. The South African market ended the week in green territory as US Federal Reserve chair Jerome Powell’s softer tone saw money rush back to emerging markets. Powell indicated that the Fed could begin withdrawing some of its easy-money policies before the end of the year, though interest rates hikes may still be some way off. Master Drilling Group is among the top performers this week. Shares in the drilling services company soared 20.3% WoW despite the fact that it revised its earnings growth expectations down. Indeed, on Thursday, the company published an updated trading statement, noting that it now expects its earnings per share (EPS) for the six months ended June 30, to increase by between 61% and 66% year-on-year to between 85.90c and 88.50c. Previously, the company anticipated an EPS increase of between 77% and 87% to between 94.70c and 100c. Shares are now up 35.73% YTD. The JSE heavyweight, Prosus, closed higher at ZAR 1,247.85 on Friday (+1.70% WoW). Shares in the tech investor are now down 22.31% YTD.

ZSE - Equities in Harare extended losses this week as the ASI declined another 1.24% WoW. Daily average turnover dropped by two thirds to around ZWL 93m (USD 1.08m) compared to ZWL 289m the week before. The total market capitalisation amounts to ZWL 802.53bn (USD 9.34bn), up 155.50% so far this year.